Page 30 - State-of-the-Industry-2013

P. 30

State OF the induStry 2013

reach of mobile money distribution networks

Thanks to widespread distribution networks, mobile money is extending access to fnancial services to more people and has become

an efective complement to the banking and payments industries. On average, there are 28.4 agent outlets per 100,000 adults globally.

this is six times more than the average density of bank branches in these markets, which stands at 4.6 per 100,000 adults. in 81% (44 out

of 54 markets) of the markets where we had respondents, there are now more mobile money outlets than bank branches. this signals

that mobile money is able to expand access to fnancial services for the unbanked and underbanked. in countries where there are more

mobile money agents than bank branches, agents rather than banks are becoming the face of the fnancial services industry.

20

With an average of 39.0% agents in rural areas in June 2013, the bulk of mobile money agents are in urban areas. it is unsurprising

21

that there are more urban agents for a number of reasons; one of them is recruitment. indeed, mobile money providers look to recruit

agents who can make the requisite monetary investments in mobile money, and who employ staf with a high level of literacy, which is

more typically found in urban areas.

Carefully identifying the right areas to put mobile money agents is critical. today, operators can use data to identify gaps in the coverage

of fnancial services and that information to select the right candidates (read text box 6 to fnd out more).

agent activity

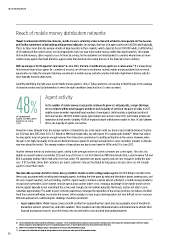

48% As the number of mobile money access points continues to grow at a dizzying rate, a major challenge

for the industry will be ensuring agent activity as well as quality of service at the point of sales. in 2013,

them are inactive. 464,000 mobile money agent outlets were active in june 2013, performing at least one

of registered mobile money providers registered large numbers of new agents. unfortunately, a signifcant portion of

agent outlets were transaction in that month. Globally, 47.6% of registered agent outlets were inactive in june. in Sub-Saharan

inactive in June

2013 africa, the majority of agents are inactive.

viewed at a more granular level, the average number of transactions per active agent outlet per day increased slightly between Septem-

ber 2012 and june 2013, from 5.6 to 6.7. Based on mmu benchmark data, any ratio above 10 is usually quite healthy . When that ratio is

22

too low, agents may not generate enough revenue from transaction commissions to justify participation in the service. however, when

the ratio is too high, the quality of the service declines because agents do not have enough time to serve customers properly or educate

new ones about the service. the average number of transactions per day is even lower for atms: only 1.0 in june 2013.

another relevant metrics to understand agent activity is the average number of active customers per active agent. this ratio also

slightly increased between September 2012 and june 2013 from 77.1 to 80.0. Based on mmu benchmark data, a ratio between 150 and

800 is probably healthy. When that ratio is too low, under 150 customers per agent, agents may not earn enough to justify the busi-

ness. if it’s too high, above 800 customers per agent, customers may get frustrated by long queues because there are not enough

agents to meet their needs.

This raises the question of whether mobile money providers should consider cutting inactive agents. the frst thing to consider is the

direct costs associated with recruiting and managing agents, including the time spent by sales and distribution teams, training costs, and

the cost of agent materials, such as branding, and POS. agents need to maintain a certain level of activity for a mobile money provider to

recoup these investments in the channel. inactive agents incur another indirect cost: creating a bad image of the mobile money service.

inactive agents typically do not understand the service well enough, do not maintain adequate foat levels, and are not able to serve

customers appropriately. this leads to poor customer experiences, damages the reputation of the service provider, and reduces the likeli-

hood the customer will adopt or promote the service. unfortunately, it is easy to get a bad reputation, but very difcult to turn it around.

diferent approaches to addressing this challenge should be considered:

• Agent segmentation: mobile money services beneft greatly from segmenting their agent base by geography, level of investment,

transaction volumes, product mix, and other variables. these analytics can help distribution teams understand how to allocate their

fnancial and human resources most efectively, keep top performers loyal, and deal with underperformers.

20. Survey respondents were asked to provide their defnition of “rural areas”. 75% of respondents defned a rural area as an area outside of the major cities in their country. Other respondents (almost 20% of the sample)

defned a rural area as areas with limited or no access to traditional fnancial services. it is unclear which criteria were used to precisely defne these areas.

21. Only 41% of respondents knew what percentage of their agents are in rural areas and provided this percentage.

22. it is important to consider this ratio along the average number of active customer per active agent and the commission structure.

24