Page 26 - State-of-the-Industry-2013

P. 26

State OF the induStry 2013

TexT BOx 4

the big PaYoff: getting customers active at registration*

Low customer activity rates have been a persistent challenge across the mobile money industry. The question every operator is

asking: How can one increase customer activity and therefore mobile money ARPUs?

One way to think about this question is asking how to maximise the value of every customer interaction. Perhaps the most

important interaction is the point of registration. Here is where a customer learns about the service, identifes how it might fll

a specifc need, and draws frst impressions.

Customers who have a positive experience at the point of registration—perhaps a sales agent who took time to thoroughly explain

the service—might be encouraged to transact on that same day. Does this extra efort to encourage a transaction on the day of

registration pay of? Let’s look at data from one anonymous operator.

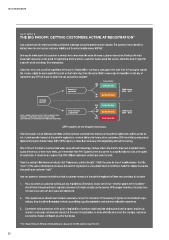

Current status

49%

Active (90-day)

Transacts at Mobile money

registration ARPU = $0.37

Inactive (90-day)

51%

Customer

Registers

39% Active (90-day)

Doesn’t transact 31% Inactive (90-day) Mobile money

at registration ARPU = $0.19

arPu = monthly average over recent 3-month Period

transact = send money, Pay Bill, or Buy airtime

data from one oPerator only, not industry Benchmark 30% Never transacted

ARPU numbers are net of agent commissions.

This data reveals a stark diference in future activity between customers that transact at the point of registration and those that do

not. Customers who transact at the point of registration are more likely to be future active customers (26% more likely) and produce

signifcantly higher mobile money ARPU (95% higher) as those that walk away after registering without transacting.

Why is this so? Consider a customer that walks away without transacting. Perhaps after a few months they have forgotten how to

access the service, or even more likely, can’t remember their PIN. Suddenly there is a barrier to usage that did not exist at the point

of registration. It should be no surprise that 30% of these customers are lost and never transact.

There is a saying in the insurance industry that “insurance is sold not bought.” Might the same be true of mobile money—that the

“push” of the sales and education process at the point of registration is a key determinant of whether a customer adopts the service

along with pure customer “pull.”

How can operators increase the likelihood that a customer transacts at the point of registration? Here are some ideas to consider:

1. Place incentives on customer activity, not just registration: The mobile money sales force—whether agents or foot soldiers—

should have strong incentives to register customers that might actually use the service. With proper incentives, the sales force

will take more care with each customer interaction.

2. Train agents how to educate and convince customers, not just the mechanics of transacting: If agents are involved with regis-

trations, they should be thoroughly trained on providing a quality registration and customer education experience.

3. Experiment with promotions at the point of registration: Operators might consider adding incentives for agents and/or cus-

tomers to encourage customers to transact at the point of registration, to strike while the iron is hot. For example, customers

can receive a bonus contingent on same-day usage.

* This article by Philip Levin (MMU) was initially published as a blog post on the MMU website on August 29, 2013.

20