Page 41 - Mobile World Daily - Day One

P. 41

Joss Gillet, ARPU | ANALYSIS

Senior Manager,

GSMA Intelligence Matthew Iji,

www.gsmaintelligence.com Forecasting Analyst,

GSMA Intelligence

Evaluating consumer

spending: the need for

a revised ARPU metric

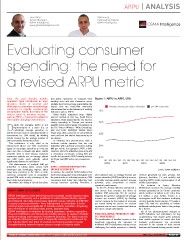

Over the past decade, mobile that allow customers to consume their Figure 1: ARPU vs ARPS, USA Source: GSMA Intelligence

operators have introduced an ever monthly voice and data allowances across

growing choice of services and multiple devices have been exacerbating the new indicator such as average revenue per revenue generated by each product line

offerings to consumers as technology impact that the multi-SIM ownership unique subscriber (ARPS) would help to more (internet, fixed-line, TV and mobile) and

continues to rapidly revolutionise phenomenon has on the relevance of existing accurately evaluate mobile markets’ revenue reporting ARPU results representative of all

consumption habits. But many of the indicators such as ARPU. potential, price competition or mobile mobile consumption.

metrics used to measure success – operators’ performance.

such as ARPU — have yet to adapt to These tariffs originated from ‘digital For instance, in Spain, Movistar

this rapidly changing environment. pioneer’ markets in Asia (e.g. South Korea, In the US, Verizon Wireless introduced a (Telefónica) measures the average monthly

Singapore, Hong Kong) and the US, and are new metric that counters the effect of revenue generated by its Fusión customers

Despite the acronym, ARPU is not slowly spreading to Europe and mature multiple SIM ownership. For its contract which reached 3.4 million in Q2 2014, from

representative of a user’s (i.e. an markets across most regions. For instance, in segment, the operator calculates the average 2.2 million a year earlier. Fusión is a

individual) average spending on the US, Verizon Wireless’ ‘More Everything’ revenue per account (ARPA) by dividing convergence tariff that combines multi-play

mobile services since it is calculated based on plan and AT&T Mobility’s ‘Mobile Share contract revenue by the number of accounts services (mobile, fixed, internet, TV) under a

connections (i.e. SIM cards), by dividing Value’ plan allow customers to use unlimited per month during the period. An account single bill, with the possibility to include

mobile revenue by the average number of voice and text and shared data across up to represents one or more connections/devices additional mobile phone lines to the package

SIM connections during the period. ten devices. that share a single subscription. for a flat fee.

THINKING AHEAD: FROM MULTI-SIM

This calculation is only valid in an To illustrate this phenomenon, take a TO CONVERGENCE All of the aforementioned changes to

environment where one SIM connection fictitious mobile operator that has one The proliferation of bundled services is also ARPU definitions and calculations are key

equals to one unique subscriber, as it was the subscriber with a primary connection costing negatively impacting the relevance of considerations that require great attention

case more than a decade ago when mobile $60 per month, the operator’s ARPU is $60. traditional ARPU calculations, making it more from mobile operators to ensure that their

networks were in their infancy. However, However, when the subscriber goes on to add challenging for mobile operators to identify business performances are accurately

consumers actively use on average almost a secondary connection costing $20 per evaluated in the context of their current

two SIM cards each globally which month, the operator’s ARPU actually reduces business and forward-looking market trends.

significantly distorts the calculation. by 33 per cent ($80 across two connections =

$40).

This phenomenon of multiple SIM per

subscriber is taking place across both ARPS = AVERAGE REVENUE PER

developed and developing regions, albeit UNIQUE SUBSCRIBER

being more prevalent in the latter as cost-

conscious consumers tend to accumulate In essence, the constant ARPU declines that

prepaid SIM cards to take advantage of the have been taking place around the globe over

latest deals and promotions. the past decade are reflecting trends at a SIM

connection level rather than reflecting ‘real’

Meanwhile, the ability of shared data plans average consumer spending. Therefore, a

ABOUT GSMA INTELLIGENCE

GSMA Intelligence is the definitive source of global mobile operator data,

analysis and forecasts; and a publisher of authoritative industry reports

and research. Our data covers every operator group, network and MVNO

in every country worldwide – from Afghanistan to Zimbabwe. It is the

most accurate and complete set of industry metrics available, comprising

tens of millions of individual data points, updated daily.

GSMA Intelligence is relied on by leading operators, vendors, regulators,

financial institutions and third-party industry players, to support strategic

decision-making and long-term investment planning. The data is used as

an industry reference point and is frequently cited by the media and by

the industry itself. Our team of analysts and experts produce regular

thought-leading research reports across a range of industry topics.

MOBILE WORLD CONGRESS DAILY 2015 | www.mobileworldcongress.com Monday 2nd March PAGE 41