Page 23 - A2A-interoperability_Online

P. 23

a2a interoperaBility makinG moBile money scHemes interoperate

3.7

commercial processor

for bank interface

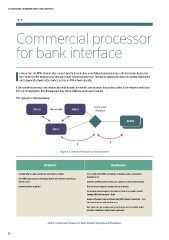

I n this option, the mmo schemes inter-connect directly to each other, using bilateral agreements (as in the first option above), but

inter-connect to the banking sector through a single commercial processor. this may be appropriate where an existing organisation

runs a payment network in the market, such as an atm network operator.

if the commercial processor has relationships with all banks in a market, and processes transactions similar to the required credit trans-

fers (e.g. bill payments), then this approach may offer a relatively quick route to market.

this approach is illustrated below:

Commercial

MMO A MMO B Processor

BANKS

MMO C

$

$

Figure 6: Commercial Processor for Bank Interface

STRENGTHS WEAKNESSES

scalable where scale is needed (i.e. interfacing to banks) loss of control for mmos on interface to banks; on price, connections,

innovations etc.

each mno gains access to all external parties who connect to processor,

and vice versa unknown additional transactions costs added by commercial third party

Bank integration simplified new settlement approach required for bank transfers

transaction reversal requests are harder as there is no specific contract

between mmo and recipient’s Bank

Danger of function creep to include inter mno scheme transactions – and

subsequent loss of control in that area

user experience for sending money from bank account to mobile wallet

account is undefined, requires bank agreement

Table 6: Commercial Processor for Bank Interface Strengths and Weaknesses

20

3.7

commercial processor

for bank interface

I n this option, the mmo schemes inter-connect directly to each other, using bilateral agreements (as in the first option above), but

inter-connect to the banking sector through a single commercial processor. this may be appropriate where an existing organisation

runs a payment network in the market, such as an atm network operator.

if the commercial processor has relationships with all banks in a market, and processes transactions similar to the required credit trans-

fers (e.g. bill payments), then this approach may offer a relatively quick route to market.

this approach is illustrated below:

Commercial

MMO A MMO B Processor

BANKS

MMO C

$

$

Figure 6: Commercial Processor for Bank Interface

STRENGTHS WEAKNESSES

scalable where scale is needed (i.e. interfacing to banks) loss of control for mmos on interface to banks; on price, connections,

innovations etc.

each mno gains access to all external parties who connect to processor,

and vice versa unknown additional transactions costs added by commercial third party

Bank integration simplified new settlement approach required for bank transfers

transaction reversal requests are harder as there is no specific contract

between mmo and recipient’s Bank

Danger of function creep to include inter mno scheme transactions – and

subsequent loss of control in that area

user experience for sending money from bank account to mobile wallet

account is undefined, requires bank agreement

Table 6: Commercial Processor for Bank Interface Strengths and Weaknesses

20